3 days ago

8

3 days ago

8

Editor’s Note: Join us on January 21, 2025 for a free State of the Robotics Industry webinar. Erik Nieves (Plus One Robotics), Ken Goldberg (UC Berkeley), Aaron Prather (ASTM), and Mike Oitzman (The Robot Report) will examine the latest market trends, cutting-edge technologies, and emerging applications shaping the future of robotics. Register here.

In October 2024, U.S. dockworkers went on strike, shutting down East Coast ports for three days and temporarily stalling shipping traffic. Automation became a particularly intense sticking point during negotiations.

Initially, union representatives requested new contractual language dictating that automation and semi-automation could not replace a single human worker. While the U.S. Maritime Alliance granted several other requests — including wage increases — this particular demand remains unmet.

This saga encapsulates the media perception surrounding labor and automation. They’re portrayed as opposed contingents, with robots often depicted as threatening the livelihood of the working class. In reality, labor and automation have always had a complex relationship, neither totally in opposition nor totally aligned, and that is likely to continue through 2025. The successful collaboration of robots and labor in the automotive manufacturing industry is instructive and reveals a path forward

The perceived labor vs. automation debate is one of a few trends that will dominate the robotics industry in 2025. Next year, we’ll also hear much about the importance of human-robot collaboration, market consolidation and the fate of robotics foundation models (RFMs).

Shifting perceptions about automation

Initial worker fears about automation are understandable. According to Oxford research, nearly half of U.S. jobs could be automated, at least in principle (47%). In the months ahead, warehouse and supply chain leaders must assuage their team’s doubts about automation. They can ease this process by involving laborers in AI and automation adoption discussions.

Successful unions in the automotive sector have shown that embracing automation while protecting worker interests is possible and beneficial for all parties involved. This model will likely become a roadmap for the logistics sector as it navigates similar changes.

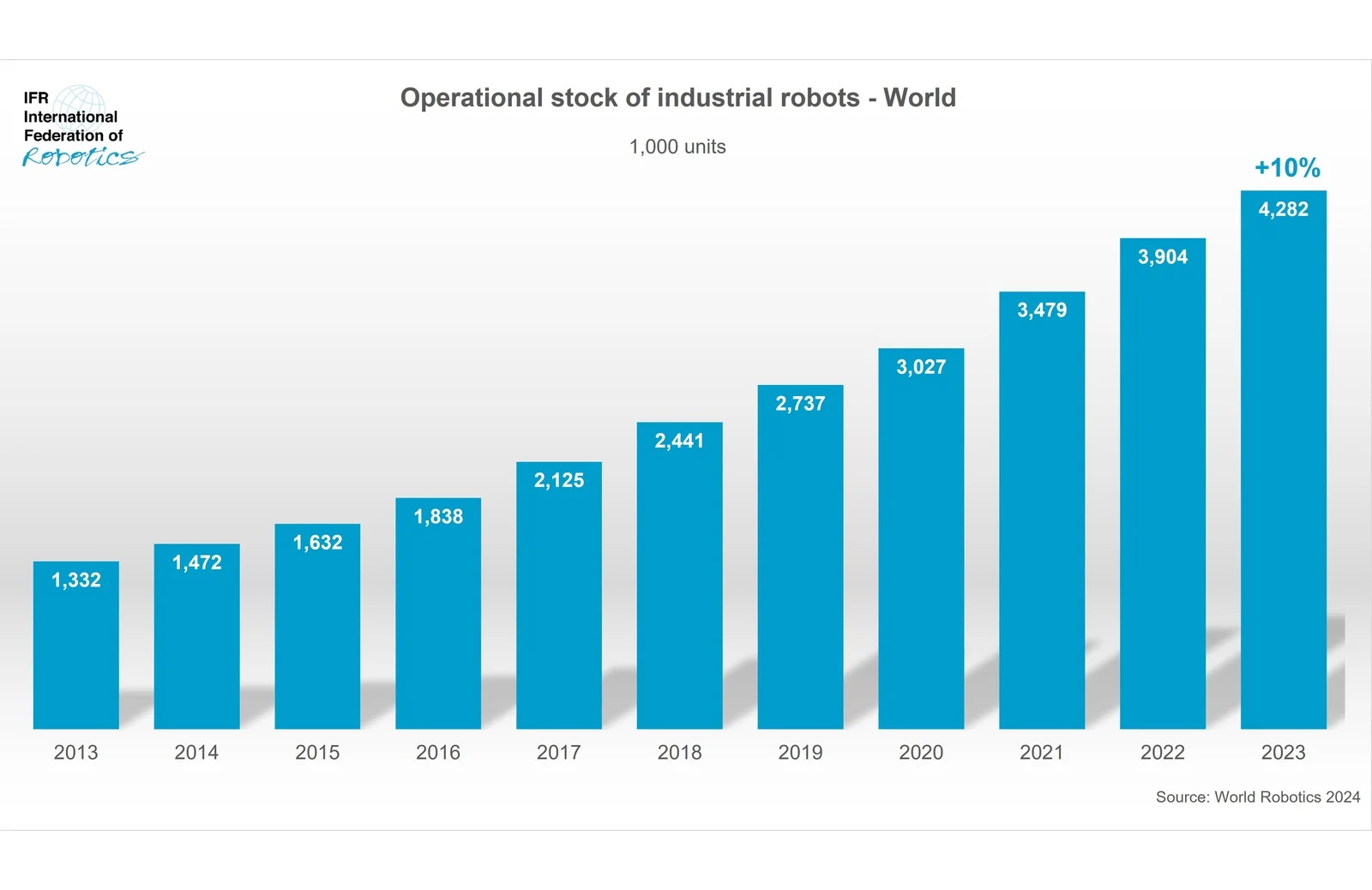

The operational stock of industrial robots worldwide. | Source: IFR World Robotics

Sustained importance of human input

With over 4.2 million factory robots deployed worldwide, some onlookers might assume we’re racing toward a fully automated future. But the reality is far more nuanced. Consider palletization and packaging, for instance — the use case most primed for automation, according to McKinsey. More than 80% of manufacturers have deployed automation for these tasks or plan to deploy it soon. Yet these applications succeed precisely because they complement rather than replace human capabilities.

On the warehouse floor, human workers remain essential for:

- Making nuanced decisions that require contextual understanding

- Quality control and oversight

- Programming and maintaining robotic systems

Thus, the most successful automation deployments will remain those that create a symbiotic relationship between human workers and robotic systems. After all, the end goal of automation isn’t to replace human work, but rather, to augment it, enabling factory workers to upskill into more rewarding roles and allowing businesses to consistently hit their throughput requirements.

Register today to save 40% on conference passes!

Register today to save 40% on conference passes!

Market consolidation and industry stability

We’ve seen an uptick in robotic applications as investments in warehouse automation increase. In particular, stationary robotics investments are on the rise, with the global robotics arm market expected to reach $84.66 billion by 2031.

This increasing interest in tried-and-true automation methods reflects a growing industry preference. Automation decision-makers are increasingly interested in working with vendors boasting a strong track record of service delivery. As a result, we’re currently seeing many companies consolidate and acquire small players to expand their bench of automation and robotics capabilities while also maintaining their existing reputation.

Thus, companies that attempt to solve incredibly niche warehouse problems are likely to struggle next year, weighed down by high burn rates and the inherent financial challenges of attracting customers in a competitive market. In contrast, full-scale automation companies concentrated on solving pervasive challenges — for example, automated depalletization in warehousing or precision robotics for healthcare and life sciences — will thrive. This is becoming even more true as companies look for vendors that can help them navigate supply chain volatility, from strikes and the increasing cost of labor to geopolitical turbulence.

Investments into robotic foundation models

Robotic foundation models (RFMs) have been (somewhat simplistically) compared to large language models for robots. They promise to broaden robots’ capabilities beyond narrow tasks and use cases to a wide range of operations, including the eventual possibility of at-home applications. Unsurprisingly, this attractive promise has gathered significant media attention and investment this year.

We’ll continue to hear about RFMs in 2025. As RFMs mature from their infancy, practitioners will need to understand a few basic things — including the timeline of this technology’s application in industrial contexts and the amount of computational power required to operate such technologies at scale.

In the meantime, intelligent automation — or, a model wherein humans work alongside robots trained on industry-specific data — will remain dominant. Time and time again, we’ve learned that human-robot collaboration can significantly improve efficiency while minimizing costs. The key to future success lies in leveraging the strengths of both humans and machines, creating a partnership that maximizes productivity without sacrificing adaptability.

English (US) ·

English (US) ·